Altfest News

Proactive Planning Can Soften Blow of Major Estate, Gift-Tax Exemption Cuts on Horizon

Proactive Planning Can Soften Blow of Major Estate, Gift-Tax Exemption Cuts on Horizon

Article

Due to the number of questions posed by our clients regarding estate planning and proposed legislation, we at Altfest Personal Wealth Management are issuing an article to help you understand potential changes and evaluate your estate planning.

By Andrew Altfest & Mike Prendergast

While nothing has been enacted by Congress yet, significant and potentially painful changes could lie ahead for clients who are counting on estates worth several million dollars being exempt from taxation upon death. This year could prove to be tremendously important for positioning yourself to deal with higher estate taxes in the not-too-distant future.

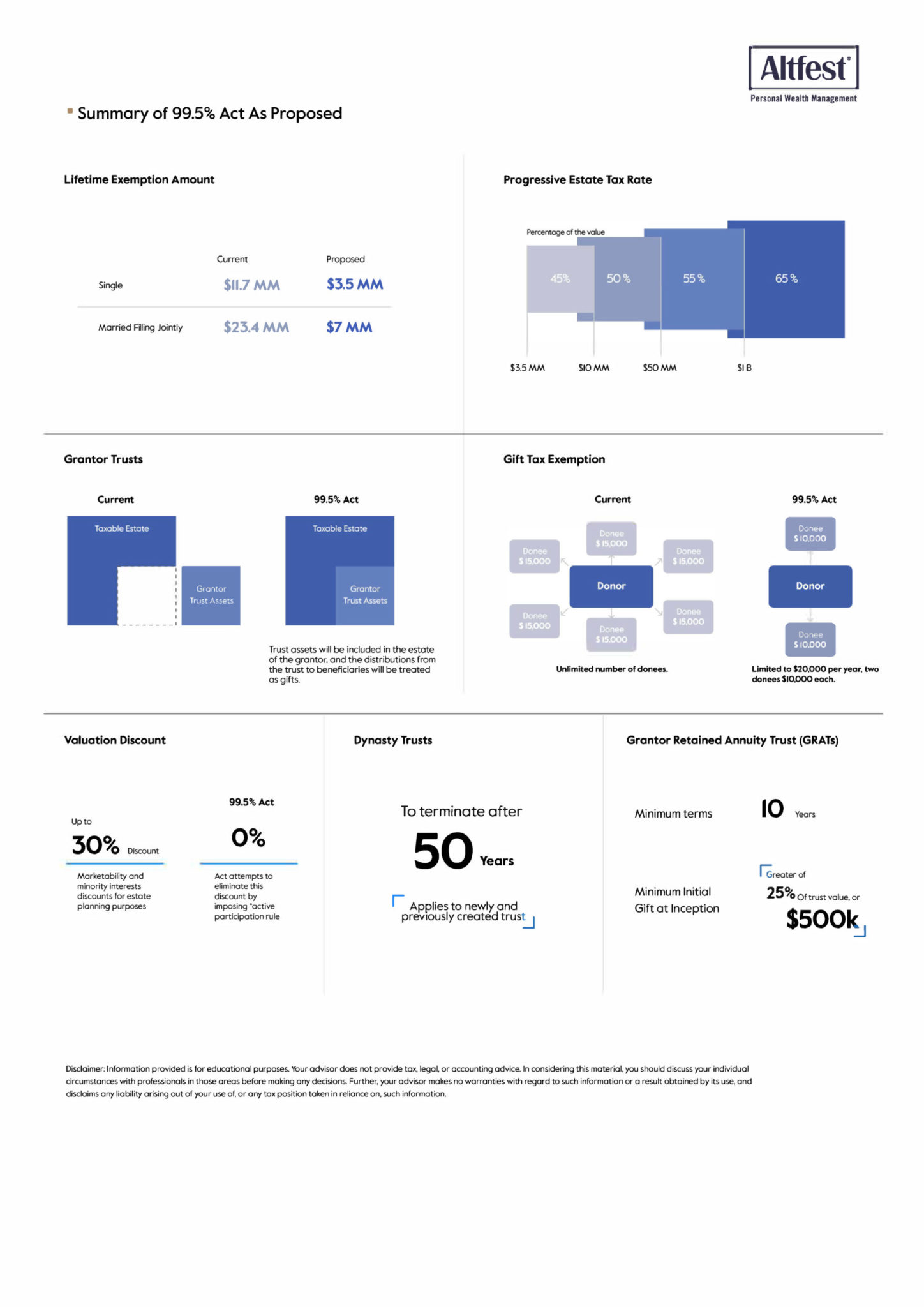

A bill introduced March 25 by U.S. Sens. Bernie Sanders (I-Vt.) and Sheldon Whitehouse (D-R.I.) aimed at addressing wealth inequality would slash the current estate tax credit, create higher tax brackets for the largest estates and raise taxes on dynasty, or generation-skipping, trusts (GSTs). The proposals in the “For the 99.5% Act” restore lower 2009 estate tax thresholds, pulling the federal[1] tax-exempt amount for an estate down drastically to $3.5 million per individual and $7 million for couples — less than one-third of the current federal exclusion levels.[2]

| Advice for Planning Now

If appropriate to your situation, consider the following strategies, which we believe could be very advantageous:

|

Anyone with assets over the proposed new exemption levels will be adversely affected, so it may be beneficial to move as soon as possible to plan for asset transfers and other tax-neutral strategies. If passed unchanged by Congress, the 99.5% Act bill would affect the estates of those dying after Dec. 31, 2021, although several measures could take effect sooner, on the date of enactment, if the bill becomes law this year.

The last 20 years have been referred to as “the golden age of estate planning” because attorneys have been able to help clients save millions of dollars through legal, well-thought-out strategies. But that opportunity may be coming to an end as soon as this year.

As most Americans are aware, in 2021, as a result of former President Trump’s Tax Cuts and Jobs Act (TCJA), we benefit from combined exemption levels of $11.7 million per individual or $23.4 million for married couples for both gift and estate taxes. And regardless of the fate of current estate tax legislation, the TCJA ends after 2025, so diminished estate tax exemptions are quite possible.

At present, significant assets can be passed on either by someone’s dying or by making gifts. But these transfers must happen before the effective date of the provisions in Sanders’ bill, if enacted.

In addition, the 99.5% Act proposal slashes the U.S. federal lifetime gift-tax exemption to $1 million, from the $11.7 million level now, for gifts made after Dec. 31, 2021. Also assets transferred to grantor trusts after the 99.5% Act becomes effective would be included in the grantor’s estate.

Other, similar legislative proposals have been floated in Congress that would lessen or remove step-up basis for valuation of inherited assets, which could be an enormous change for many. The tax burden of a large inheritance is usually eased by using the higher, or “stepped-up,” current market value of the asset at the time of inheritance for income tax purposes to minimize the beneficiary’s capital-gains tax bill. If some of the changes under review in Congress now become law, this provision would disappear.

Here’s how the bill’s changes would affect the following levels of taxable estate and gift assets:

|

Estate and Gift Value (for individuals) |

Current Tax Rate |

Proposed Tax Rate |

| $1 million to $3.5 million (gifts only) | 40% | 45% |

| $3.5 million to $10 million | 40% | 45% |

| $10 million to $50 million | 40% | 50% |

| $50 million to $1 billion | 40% | 55% |

| In excess of $1 billion | 40% | 65% |

Please see the image below for a summary of key parts of the legislation.

Establish a Trust for the Future

You can establish or adjust a trust now to shield assets from higher estate tax in the future. Acting soon is critical because it could be a “use-it-or-lose-it” situation.

Trusts can work and protect in many life situations, from elderly parents, to children and your future generations, to divorce, to unforeseen creditor claims and financial difficulties.

If you set up a grantor trust now, the trust itself does not have to pay income taxes. Instead, the grantor or originator pays them. As an individual, the grantor has far more favorable income tax rates than does a trust, where the tax rates are severely compressed. For irrevocable grantor trusts, under current law, the grantor is seen as the owner for income and capital gains tax purposes, but not for estate tax purposes. There are several types of these trusts, which your Altfest financial advisor, tax or estate attorney can explain in greater detail.

Estate planning experts we have spoken to advise doing something now, or at least getting ready to do so, including getting your attorneys thinking about it. Depending on your situation, you can have a draft plan drawn up without delay, and for clients to be prepared to make a wealth transfer in the remaining months of 2021.

If it looks like Congress is going to pass this legislation, get in under the wire to protect your assets later. Do something sooner rather than later to set up your irrevocable grantor trust, spousal lifetime access trust (SLAT) or possibly a dynasty trust.

Speak with a Financial Professional

Planning for the proposed changes from Congress and how they might affect your estate, large gifts and taxes can be overwhelming. Feel free to contact us and, of course, your legal advisor for help in understanding the benefits of a new estate plan in accordance with the new legislation to help shape and realize financial goals.

Disclaimer: Information provided is for educational purposes. Your advisor does not provide tax, legal, or accounting advice. In considering this material, you should discuss your individual circumstances with professionals in those areas before making any decisions. Further, your advisor makes no warranties with regard to such information or a result obtained by its use, and disclaims any liability arising out of your use of, or any tax position taken in reliance on, such information.

[1] While this is at the federal level, some states, including New York, impose state estate taxes, which also need to be addressed.

[2] https://www.thinkadvisor.com/2021/03/25/sen-sanders-introduces-estate-tax-bill-with-brackets/

Investment advisory services provided by Altfest Personal Wealth Management (“APWM”). All written content on this site is for information purposes only. Opinions expressed herein are solely those of APWM, unless otherwise specifically cited. Material presented is believed to be from reliable sources and no representations are made by our firm as to another parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation.

All investing involves risk, including the potential for loss of principal. There is no guarantee that any investment plan or strategy will be successful.