Altfest Insights

Health-care professionals need special attention when it comes to asset protection

Health-care professionals need special attention when it comes to asset protection

Article

By Ekta Patel CFP®, MBA, Director, Advisor, Altfest Personal Wealth Management

Added to the many professional stresses of being a busy physician today is the threat of a financially devastating malpractice lawsuit. Most practicing doctors are already familiar with the costly but essential step of maintaining malpractice insurance. I’d like to recommend some other ways to protect yourself against potential legal actions that you may not have thought about.

As the head of financial planning and a director at Altfest Personal Wealth Management, I advise our numerous physician clients to consider a range of creditor protections after securing adequate malpractice insurance. Here are some of the approaches you should be familiar with to effectively shield your hard-earned assets.

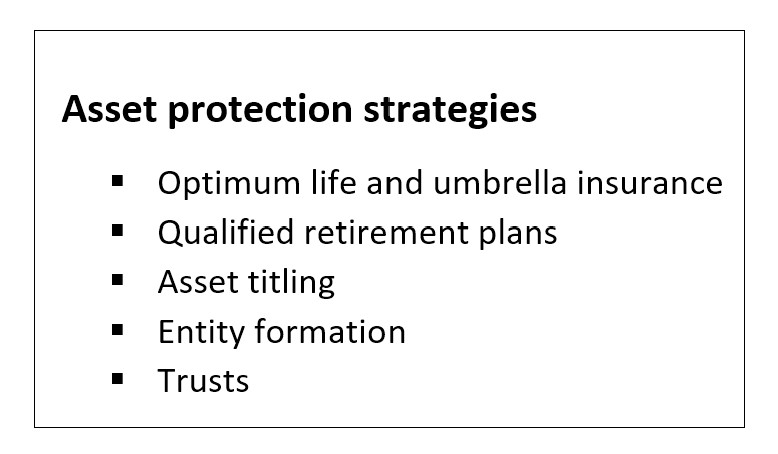

Optimum life and umbrella insurance. Think of everything I suggest as a form of risk management that can reduce the amount of your assets that are exposed to potential legal action. One strategy among these is for physicians to work with an insurance advisor to determine how best to ease the financial consequences for your loved ones if you died. We regularly help our clients connect with such auxiliary service providers with the goal of shielding their assets appropriately.

The life insurance process starts with evaluating your and your family’s needs in the short and long terms. Then the insurance professional would assess the value of your estate and what burden of state and federal estate taxes it might bring. The life insurance policy might be structured to cover that estate tax bill when you pass on, for example. We also urge our physician clients to set up an “umbrella” insurance policy for coverage in the event of a non-malpractice related lawsuit. As doctors are often perceived to be deep-pocketed targets, an umbrella, or excess liability, policy can protect your assets in such situations – it picks up coverage where your auto or home insurance policies leave off.

Qualified retirement plans. Although participating in your employer’s retirement plan is an obvious step toward being financially secure when your career ends, it’s also a way to gain state and federal asset exemptions. U.S. laws exist to protect retirement savings from creditors, so we can work with our clients to maximize their contributions to the right kinds of retirement plans to shelter that money from creditor seizure.

As you may know, the Employee Retirement Income Security Act (ERISA) covers most employer-sponsored retirement plans, including 401(k) plans, pension plans and some 403(b) and 457 plans. Even if you, as a physician, have accumulated millions of dollars in your retirement account, creditors usually cannot access funds in ERISA-qualified plans. Individual retirement accounts (IRAs) receive some but more limited asset protection under law.

Asset titling. Unfamiliar with this technique? It’s a legal step that’s among the simpler options for asset protection. I often tell clients to consider one called tenancy by entirety. It’s a way for married couples to hold equal interest in real estate or other real property, as well as survivorship rights to keep their property out of probate. But it’s not the same as 50/50 ownership.

With this type of titling, each spouse owns 100% of the property. As such, it protects your home or your other real estate from the doctor spouse’s creditors. A creditor cannot force the split-up of such a titling, so cannot reach the money. It’s worth considering if it’s available in your state.

Entity formation. Your medical practice may already be structured as a corporation or limited liability company (LLC). Did you know you can do something similar with your personal assets to gain protection from judgments, whether external lawsuits, such as a malpractice action, or a personal lawsuit? For instance, if you own rental property, you might establish an LLC for it to shield those assets from a tenant lawsuit. A family limited partnership (FLP) may be another suitable option, in some cases.

Trusts. Last, we frequently connect our physician clients with attorneys who can set up asset protection trusts for them. These are types of irrevocable trusts that allow you to transfer assets, thereby giving up control and ownership of the assets, but retaining the ability to receive distributions from the trust. This is probably your ultimate asset protection tool.

It’s important to note that if you are an income beneficiary of a trust, the distributions are made at the discretion of the trustees and are not mandatory. So, to the extent that you don’t have to take the distributions out of the trust, that money is not accessible to creditors. But be aware it’s one of the more expensive and labor-intense techniques for shielding your assets.

Let us review your creditor protection

I invite you to learn more about how my firm, which has advised health-care professionals for decades, might be able to improve your finances’ protection from legal actions. If you have specific questions, please book some time for a complimentary consultation.

Investment advisory services provided by Altfest Personal Wealth Management (“APWM”). All written content on this site is for information purposes only. Opinions expressed herein are solely those of APWM, unless otherwise specifically cited. Material presented is believed to be from reliable sources and no representations are made by our firm as to another parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation.

All investing involves risk, including the potential for loss of principal. There is no guarantee that any investment plan or strategy will be successful.